So wind decided to go full lumberjack on your house? Classic. Trees and branches don’t just fall—they make dramatic entrances, smashing into roofs, walls, and anything else that dares to exist in their way. Roof punctures? Check. Wall damage? Oh yeah. Even your foundation might take a hit if the tree was feeling extra spicy. 🌀🌳

But wait, there’s more! Broken windows? Damaged siding? Now your home’s just an open invitation for water to waltz in and start a moldy little rave. And let’s not forget the giant, splintery debris blocking your driveway or turning your yard into an obstacle course of danger.

How to stop Mother Nature’s wooden missiles from turning your roof into their personal crash pad? Here’s how to outsmart those branches before they decide to drop in unannounced:

Do this, and your roof won’t have to play defense against falling trees every time the wind acts up.

Mother Nature might be stubborn, but science has a few tricks up its sleeve. Check this out:

Embrace the tech, keep your trees in check, and let your house be the fortress it was born to be.

Don’t worry, here’s how the pros fix this leafy disaster faster than I can insult an insurance adjuster:

Boom—roof fixed, house happy, and you’re back to living your best, branch-free life.

For minor damage—like a couple of cracked shingles or a small hole—you’re looking at $200 to $800. That’s the “oops, Mother Nature sneezed” budget.

For moderate damage, where the branch went full diva and smashed a section of your roof, you’re in the $1,000 to $25,000 range. This is the “Okay, this is starting to hurt” level of repairs.

But if the branch was basically the size of a small tree and took out a big chunk of your roof, framing, or even your gutters? You’re staring down $15,000 to $150,000+. Congrats, you’re now funding your contractor’s vacation in Maui.

Oh, and if that branch caused some bonus chaos—like water damage, insulation issues, or a new indoor waterfall—those costs can climb even higher. We’re talking full home rebuild if your luck is really that bad.

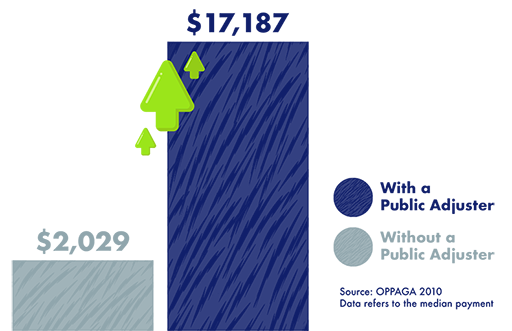

Pro tip: Call in a Public Adjuster to help you get the most out of your insurance claim so you don’t have to fund this mess out of pocket.

Roof shingle wind destruction falls squarely under the "windstorm" peril in your property insurance policy. Yep, your insurance company actually acknowledges that wind likes to rage harder than me at an all-you-can-eat wild game bar.

When wind rips shingles off your roof, tosses them into your neighbor’s yard, or just leaves your house looking like it had a bad breakup, your homeowners insurance steps in to clean up the mess. Bonus points: if water sneaks in through those missing shingles and causes damage, that’s usually covered too. Because wind doesn’t just stop at "messy"—it likes to go full chaos.

BUT—and this is a "but" bigger than my ego—if your policy has a windstorm deductible (spoiler: it probably does), you’ll be footing part of the repair bill before your insurer says, “Fine, we’ll help.” And if your roof was already falling apart before the wind showed up? Yeah, your insurance adjuster’s about to hit you with the dreaded “pre-existing damage” denial.

Homeowners Insurance: Most homeowners policies—like the HO-3 , HO-5 , HO-7 — cover it under "falling object" peril but may be combined with windstorm damage peril coverage. Yep, your insurance company actually thought, “Hey, let’s cover it when gravity teams up with a tree to ruin someone’s day.” Just make sure that branch wasn’t from your neglected, half-dead tree, or your insurer might hit you with the dreaded “denial of coverage” shrug.

Reminder that the standard homeowner insurance polices HO-1, HO-2, and HO-8 offer limited coverage compared with HO-3 , HO-5 and HO-7.

Commercial Property Insurance: Own a business? Commercial property insurance has you covered for tree branch damage to your building, roof, or signage. Plus, if the damage shuts you down for a bit, you might get business interruption coverage. Fancy!

Renters Insurance (HO-4): Renters, you’re off the hook for roof damage—it’s your landlord’s problem. Your policy, however, will cover your stuff if the branch lets water in and drowns your couch in sadness.

Condo Insurance (HO-6): For condo dwellers, your HO-6 policy will cover damage inside your unit if a tree branch creates a skylight you didn’t ask for. But the roof itself? That’s the HOA’s circus and their monkeys. Let them sweat it.

Landlord Insurance: If you’re renting out the place and a branch decides to ruin the vibe, landlord insurance covers structural damage, including the roof. Your tenants’ ruined gaming console? That’s what their renters insurance is for. Not your circus, not your monkeys.

Bottom line? If a tree branch smacks your roof, most property insurance policies will handle it—as long as you weren’t slacking on tree maintenance.

Get a free insurance policy review with a Tiger Adjusters® Public Adjuster!

Wind can uproot trees or break branches, causing them to fall on homes and result in serious structural damage. A fallen tree or branch can puncture the roof, damage walls, or even compromise the foundation depending on the impact's severity. Broken windows and damaged siding are also common, leaving the home vulnerable to water infiltration and further weather-related issues. Additionally, the debris from the tree or branch may block access points or create safety hazards for occupants. Prompt removal and repair are essential to prevent further complications, such as mold growth or structural instability.

Each year, 1 in every 20 insured homes file an insurance claim with 98% involving property damage.

(Insurance Information Institute, 2021. Claim average from 2017-2021.)

Public Adjusters are licensed insurance professionals trained to interpret your policy, scope and estimate losses, submit your claim, and negotiate with your insurance company to ensure maximum settlement amounts.