Oh, wind and roofs—the ultimate dysfunctional relationship. Wind doesn’t just gently ruffle shingles like a romantic comedy; it goes full Fast & Furious, tearing stuff up like it’s auditioning for an action flick. Shingles? Lifted, torn, and yeeted into the neighbor’s yard, leaving your roof’s underbelly totally exposed for water to move in and party. 🌀🔨🏠

But wait, there’s more! Wind loves bringing its buddies—branches, trash cans, and random debris—to puncture, dent, and generally wreck your roof’s integrity. And if the wind’s feeling extra spicy, it’ll rip off entire sections of roofing or mess with the framework like it’s showing off its strength at a gym.

Here’s how to armor up and keep those shingles where they belong—on your roof, not in your neighbor’s yard:

Do these things, and your roof will laugh in the face of windstorms while your neighbors scramble to pick up their shingles from the street.

Welcome to the future, where science and shingles team up to slap wind in the face. Here’s the cutting-edge gear you need:

With these innovations, your roof won’t just survive a windstorm—it’ll thrive.

Has the wind decided to yeet your shingles into the neighbor’s yard? No problem—here’s how the pros replace your roof faster than I can insult an insurance adjuster:

Fix wind damage fast, or your roof will go from "slightly messy" to "total disaster" in no time.

For minor damage—a few cracked shingles that need replacing—you’re looking at $200 to $600. That’s the “wind just wanted to mess with you a little” tier.

For moderate damage, where entire sections of shingles need replacing, you’re in the $1,000 to $10,000 zone. This is the “wind got tipsy and went full party mode” tier.

But if we’re talking severe damage, where the wind ripped off half your roof or exposed the underlayment to water damage, you’re staring down $15,000 to $30,000+. Welcome to the “congrats, you’re funding your roofer’s next tropical vacation” level.

Oh, and if you’ve got fancy-schmancy shingles, like custom or high-end materials? That bill can skyrocket past $13,000+. Yeah, windstorms aren’t just scary—they’re expensive.

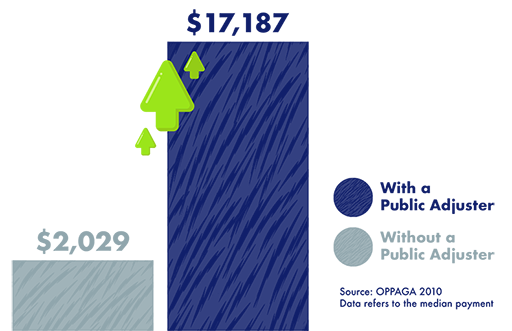

Pro tip: Call in a Public Adjuster to help you get the most out of your insurance claim so you don’t have to fund this mess out of pocket.

Roof shingle wind destruction falls squarely under the "windstorm" peril in your property insurance policy. Yep, your insurance company actually acknowledges that wind likes to rage harder than me at an all-you-can-eat wild game bar.

When wind rips shingles off your roof, tosses them into your neighbor’s yard, or just leaves your house looking like it had a bad breakup, your homeowners insurance steps in to clean up the mess. Bonus points: if water sneaks in through those missing shingles and causes damage, that’s usually covered too. Because wind doesn’t just stop at "messy"—it likes to go full chaos.

BUT—and this is a "but" —if your policy has a windstorm deductible (spoiler: it probably does), you’ll be footing part of the repair bill before your insurer says, “Fine, we’ll help.” And if your roof was already falling apart before the wind showed up? Yeah, your insurance adjuster’s about to hit you with the dreaded “pre-existing damage” denial.

Homeowners Insurance: Most homeowners policies—like the HO-1, HO-2, HO-3 , HO-5 , HO-7 and HO-8, — cover it under windstorm damage peril coverage. They’ve got your back for wind damage, whether it’s a couple of shingles gone missing or your roof’s auditioning for Extreme Makeover: Disaster Edition. Just watch out for that windstorm deductible—because, of course, the insurance world can’t resist throwing in a little plot twist.

Reminder that the standard homeowner insurance polices HO-1, HO-2, and HO-8 offer limited coverage compared with HO-3 , HO-5 and HO-7.

Commercial Property Insurance: Got a business? Commercial property insurance steps in to handle wind damage to your building, including those flung shingles. Because nothing says “bad for business” like a holey roof.

Renters Insurance (HO-4): Renters, you’re off the hook for roof shingles. Your policy only cares about your stuff inside. The roof? That’s your landlord’s circus—and their flying shingles.

Condo Insurance (HO-6): If you’re living the condo dream, your HO-6 policy covers interior damage from wind-related leaks. The roof shingles themselves? That’s the HOA’s problem. Let them deal with the drama.

Most standard property insurance policies cover wind damage. Just make sure your deductible doesn’t leave you crying harder than your roof after the storm.

Get a free insurance policy review with a Tiger Adjuster Public Adjuster!

Wind can cause significant damage to roofs, ranging from minor issues like displaced shingles to severe structural problems. High winds can lift and tear shingles, exposing the underlying layers to water damage. Debris carried by wind, such as branches or objects, may puncture the roof or weaken its integrity. In extreme cases, gusts can strip large sections of roofing material or even compromise the framework. Such damage, if not promptly repaired, can lead to leaks, insulation problems, and costly long-term deterioration.

Each year, 1 in every 20 insured homes file an insurance claim with 98% involving property damage.

(Insurance Information Institute, 2021. Claim average from 2017-2021.)

Public Adjusters are licensed insurance professionals trained to interpret your policy, scope and estimate losses, submit your claim, and negotiate with your insurance company to ensure maximum settlement amounts.