When water inside the faucet or connected pipes freezes, it expands like it’s trying to flex on you. What happens next? Crack! Your faucet or nearby pipes throw in the towel, turning into a leaky mess once the ice thaws. And that water? Oh, it’s not just dripping—it’s flooding, soaking your walls, ruining your foundation, and giving your landscaping a very unwanted bath.

But wait, there’s more! Leave that moisture hanging around too long, and you’ll be hosting a mold growth convention or weakening your home’s structure faster than a bad plot twist. ❄️🛠️💦

Here’s how to prevent icy little saboteurs and keep those faucets in line:

Follow these steps, and your outdoor faucet will stay chill—but not too chill.

Welcome to the techy side of winter! Here are the innovations ready to save your pipes—and your wallet:

Winter-proofing your faucet has gone full tech. Pick your gadget, let the tech do its thing, and tell freezing damage to shove it.

Here’s how the pros will slap a Band-Aid (or a brand-new faucet) on your frosty mess:

Frozen faucet repairs are a pain, but they’re avoidable. Wrap those pipes, insulate the faucet, and maybe don’t let winter bully your plumbing next time.

For minor damage—like replacing the faucet itself—you’re looking at $150 to $300. This is the “you caught it early, congrats on adulting” tier.

But if the ice gremlins took things further and cracked some pipes behind the faucet, now you’re in the $300 to $1,000 range, depending on how deep the damage goes and how much wall-cutting or pipe-patching the pros have to do.

And if your frozen faucet decided to turn into a water park and flood your foundation, walls, or basement? Oh baby, now we’re talking $5,000+, especially if you have water damage, mold remediation, or structural repairs on the menu. Welcome to the big leagues of pain.

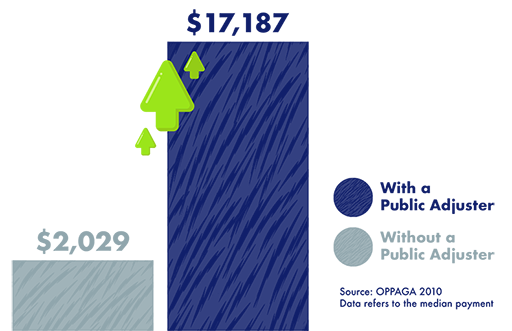

Pro tip: Call in a Public Adjuster to help you get the most out of your insurance claim so you don’t have to fund this icy mess out of pocket.

Typically frozen faucet damage falls under the "freezing" peril in some homeowners insurance policies. If water inside your outdoor faucet or pipes freezes, causing them to crack or burst, most homeowners insurance policies will cover the damage—but only if you played the responsible adult card.

Here’s the catch: if your insurer decides you were negligent—like not draining the faucet, failing to insulate it, or treating your home like an ice castle—they might hit you with the dreaded “claim denied” faster than you can say, “But it wasn’t my fault!”

Now, if the frozen faucet damage causes water leaks that flood your walls, foundation, or basement, you might also be covered under water damage—again, as long as it’s sudden, accidental, and not the result of long-term neglect.

When property damage is caused by not one, but two or more factors at the same time, its called concurrent causation. Think of it like a chaotic duet of destruction, where both causes are singing lead. Here’s the catch: one cause might be covered by your insurance policy, while the other might not.

Some states follow the anti-concurrent causation clause, which means if an excluded peril (like flooding) is involved at all, they might deny the whole claim. Other states lean toward the proximate cause rule, where the damage is covered if the dominant cause is a covered peril.

In states rocking the proximate cause rule, these Public Adjusters make sure that if a covered peril (like wind) caused the main chaos, you’re getting PAID—even if something sneaky (like flooding) decided to join the destruction party. They dig through the wreckage, connect the dots, and slap that insurer with a "nice try, pay up" notice.

But wait, it gets better! Even in states with anti-concurrent causation clauses—aka "Sorry, not covered because something uncool like flooding got involved"—Public Adjusters don’t back down. They break it all down, piece by piece, to prove which damages are tied to the covered peril. They’re like Sherlock Holmes but with spreadsheets and a vengeance.

Homeowners Insurance: Some homeowners policies—like the HO-3 , HO-5 and HO-7, — cover it under the freezing peril or the weight of ice, snow or sleet peril cover damage caused by freezing water if you’ve been a responsible adult and maintained your home. Translation: if you left your gutters clogged or didn’t keep your house warm enough, your insurer might hit you with a “LOL, not covered.”

Reminder that the standard homeowner insurance polices HO-1, HO-2, and HO-8 offer limited coverage compared with HO-3 , HO-5 and HO-7.

Commercial Property Insurance: For business owners, commercial property policies typically can cover iced gutter and frozen downspout damage too. But again, insurers are sticklers for maintenance.

Renters Insurance (HO-4): Your policy covers the cost of replacing personal belongings that are damaged. The building itself? That’s your landlord’s problem (assuming they have insurance, which, fingers crossed, they do).

Condo Insurance (HO-6): If you’re in a condo, your HO-6 policy will cover the damage to your unit’s interior—like cabinets, appliances, and personal belongings. Anything outside your unit? That’s on the condo association’s master policy.

Frozen faucet damage is usually covered under freezing peril, but only if you weren’t asking for it by letting Jack Frost take over your plumbing.

Get a free insurance policy review with a Tiger Adjusters® Public Adjuster!

An outdoor frozen faucet can cause significant damage to property when the water inside the faucet or connected pipes freezes and expands. This expansion can lead to cracks in the faucet or nearby plumbing, causing leaks once the ice thaws. Water from a broken faucet or pipe can flood surrounding areas, damaging walls, foundations, and landscaping. Prolonged exposure to moisture may also lead to mold growth or structural weakening. Promptly addressing frozen faucets and ensuring proper insulation during cold weather are essential to preventing costly property damage.

Each year, 1 in every 20 insured homes file an insurance claim with 98% involving property damage.

(Insurance Information Institute, 2021. Claim average from 2017-2021.)

Public Adjusters are licensed insurance professionals trained to interpret your policy, scope and estimate losses, submit your claim, and negotiate with your insurance company to ensure maximum settlement amounts.