A kitchen fire—the ultimate way to upgrade your cooking show into a full-blown disaster. First, flames come in hot, charring cabinets, countertops, and appliances like they’re starring in a barbecue-themed nightmare. Bye-bye, kitchen—hello, massive replacement bills!

Next, smoke spreads faster than office gossip, leaving your walls, ceilings, and furniture coated in soot and smelling like a campfire that went horribly wrong. Then there’s the heat—melting and warping everything nearby, from your floors to your wiring, just to keep things spicy. Oh, and the water or foam from putting it out? That’s the grand finale, soaking your floors and weakening your structure like a bad plot twist. 🔥🍳🛠️

Here’s the Troy Tiger approved checklist for not turning your kitchen into a fire hazard:

Follow these tips, and your kitchen will stay a place for cooking, not for chaos. Unless you burn toast on purpose. Then, well, you’re on your own.

New innovations to stop your kitchen from going all Hell’s Kitchen? You betcha! Tech geniuses have been busy whipping up gadgets to keep your culinary disasters from becoming actual disasters. Check these out:

With these innovations, you’ll be cooking smarter, not burnier. And hey, maybe even Gordon Ramsay would approve.

Ah, kitchen fire damage repair—a process as painful as watching someone burn a steak. Here’s how the professionals turn your crispy chaos back into a functional kitchen:

Once it’s all done, you’ll have a fresh, fire-free kitchen ready for action.

Brace yourself, because fixing kitchen fire damage is gonna sting. On average, you’re looking at $3,000 to $15,000 for minor to moderate damage—like cleaning up smoke, replacing a few cabinets, or fixing heat-damaged appliances. But if your kitchen went full-on inferno and the fire decided to redecorate with ashes? That price skyrockets to $20,000 to $50,000+, especially if walls, flooring, or wiring need repairs or replacing.

And let’s not forget the hidden villains: smoke damage spreading through your house or water from extinguishing the fire soaking into everything. Those can add thousands to the tab. Moral of the story?

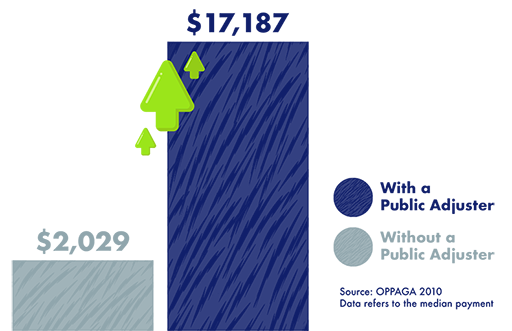

Call in a Public Adjuster to help wrangle your insurance claim, or you might end up footing more of the bill than you’d like.

Kitchen fire damage? That fiery fiasco falls under the fire or lightning peril in your property insurance policy. It’s part of the standard coverage in most homeowners and commercial property insurance policies. Whether your stove decided to audition as a flamethrower or your frying pan went rogue, the fire peril has your back for flames, heat, and even the smoky aftermath.

Now, here's the fine print twist: if the fire happened because you left oil unattended or decided to clean your oven with a flamethrower (creative, but no), your insurer might scream "negligence!" and try to deny your claim. But as long as it wasn’t your fault, fire damage is typically covered. So, congrats! Your crispy kitchen chaos gets the insurance nod.

Pro tip: if the fire causes smoke damage, that’s usually covered too—it’s like a bonus round of misery that your policy handles. But here’s the catch: if your insurer thinks it’s your fault because of negligence, they might pull a "not covered" card faster than you can say, "I smell smoke."

Homeowners Insurance: All homeowners policies—like the HO-3 , HO-5, HO-7, HO-8—cover fire damage. Whether your frying pan turned into a bonfire or your oven decided to cosplay as a dragon, you’re covered for structural damage and personal belongings. Just make sure you didn’t cause the fire through negligence, or your insurer might hit you with a "nice try" denial.

Reminder that the standard homeowner insurance polices HO-1, HO-2, and HO-8 offer limited coverage compared with HO-3 , HO-5 and HO-7.

Commercial Property Insurance: For business owners, commercial property policies typically cover fire damage to the building, equipment, and inventory. So, if your restaurant’s kitchen decided to flame out, you’re covered—as long as you didn’t cut corners on safety or inspections.

Renters Insurance (HO-4): Good news for renters—your policy covers the cost of replacing personal belongings damaged by the fire. The building itself? That’s your landlord’s problem (assuming they have insurance, which, fingers crossed, they do).

Condo Insurance (HO-6): If you’re in a condo, your HO-6 policy will cover the damage to your unit’s interior—like cabinets, appliances, and personal belongings. Anything outside your unit? That’s on the condo association’s master policy.

In short, as long as you’ve got a solid policy and didn’t start the fire by, say, trying to flambé in a polyester onesie, insurance has your back.

Get a free insurance policy review with a Tiger Adjusters® Public Adjuster!

A kitchen fire can cause extensive property damage by charring cabinets, countertops, and appliances, often requiring complete replacements. Smoke from the fire can spread throughout the home, leaving soot and odors on walls, ceilings, and furniture. The intense heat can warp or melt nearby materials, including flooring and electrical wiring, posing additional safety risks. Water or foam used to extinguish the fire may cause secondary damage, such as waterlogged floors and structural weakening. Prompt cleanup and restoration are essential to mitigate further damage and ensure the home is safe for occupancy.

Each year, 1 in every 20 insured homes file an insurance claim with 98% involving property damage.

(Insurance Information Institute, 2021. Claim average from 2017-2021.)

Public Adjusters are licensed insurance professionals trained to interpret your policy, scope and estimate losses, submit your claim, and negotiate with your insurance company to ensure maximum settlement amounts.