Strong winds and siding—a match made in destruction heaven. When the wind decides to throw a tantrum, it rips siding off your house like it’s peeling an onion. What’s left? A sad, exposed structure just begging for moisture and temperature drama to move in rent-free. 🌀🏠💥

But wait, there’s more! Wind doesn’t come alone—it brings its backup singers: flying debris. These wannabe missiles can dent, crack, or straight-up puncture your siding, leaving your house looking like it lost a fight with a meteor shower. Vinyl siding? Cracks faster than a cheap phone screen. Wood siding? Splits, warps, and starts looking like it’s auditioning for a horror movie.

And when your siding’s gone AWOL, water sneaks in, inviting mold to the party and whispering sweet nothings to structural damage. The fix? Inspect and repair that siding ASAP, or kiss your energy efficiency—and your wallet—goodbye. Your house deserves better than looking like it survived a wind-powered apocalypse.

Here’s how to armor up your house and tell wind to take a hike:

Follow these steps, and your house will stand tall while the wind huffs, puffs, and sulks because it couldn’t blow your siding down.

Welcome to the world of next-level wind-proofing, where science and tech team up to win against wind siding damage.

With these innovations, your siding will be tougher than a blockbuster villain—and way better looking.

Here’s how the pros clean up this hail siding damage :

And there you have it! Your siding’s back in action, ready to laugh in the face of the next gusty tantrum Mother Nature throws.

For minor damage—a few cracks or dents that can be patched or painted over—you’re looking at $200 to $600. That’s the "wind gave your house a love tap" budget.

For moderate damage, where sections of siding need replacing, it’s gonna cost you $1,000 to $3,000. Welcome to the "wind was feeling spicy" tier.

But if the wind decided to go full 'Smash', leaving your siding looking like Swiss cheese and messing with your house’s underlying structure? You’re staring down $5,000 to $10,000+. Yep, that’s the "thanks for the house remodel, Mother Nature" level.

And if you’ve got fancy, custom, or high-end siding? Buckle up, because the price can hit $15,000+. At that point, you’re basically funding your contractor’s next Caribbean getaway.

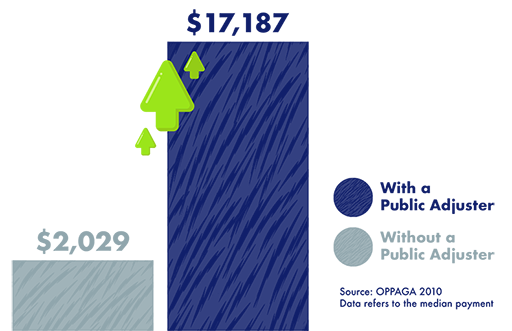

Pro tip: Call in a Public Adjuster to help you get the most out of your insurance claim so you don’t have to fund this mess out of pocket.

The frosty assault of home siding hail damage falls squarely under the "windstorm" peril in your property insurance policy. Yep, your insurance company actually planned for the wind to throw a hissy fit and rip your siding off like it’s peeling a banana.

Bonus points if water sneaks in because of the damage—that’s usually covered too. Because, hey, why stop at just one problem?

BUT—and it’s a big ol’ but—you might have a windstorm deductible to deal with first. That’s the “fun” part where you pay out of pocket before your insurance actually starts coughing up the cash. Oh, and if your siding was already a cracked, brittle mess before the wind showed up? Yeah, your insurer might hit you with the dreaded “neglect” denial.

Homeowners Insurance: Most homeowners policies—like the HO-1, HO-2, HO-3 , HO-5 , HO-7 and HO-8 — cover it under windstorm damage peril coverage. Just be ready for that wind/hail deductible, because insurance companies love reminding you that nothing in life is free.

Reminder that the standard homeowner insurance polices HO-1, HO-2, and HO-8 offer limited coverage compared with HO-3 , HO-5 and HO-7.

Commercial Property Insurance: Got a business with a building? Commercial property insurance will cover wind damage to siding, windows, and anything else the wind decides to bully. Bonus: if the damage disrupts your operations, you might get some business interruption coverage too. Fancy.

Renters Insurance (HO-4): Sorry, renters—your policy doesn’t care about siding. It’s all about protecting your stuff inside the house. The exterior? That’s your landlord’s problem, so sit back and let them deal with the drama.

Condo Insurance (HO-6): Living the condo dream? Your HO-6 policy covers interior damage if wind wrecks the siding and water sneaks in. The siding itself? That’s the HOA’s circus—better hope their master policy is up to snuff.

Most property insurance policies will step in when wind decides to throw down with your siding—just make sure your deductible doesn’t leave you crying into your repair bill.

Get a free insurance policy review with a Tiger Adjusters® Public Adjuster!

Strong winds can loosen or rip off sections of home siding, exposing the structure to moisture and temperature fluctuations. Flying debris carried by wind can dent, crack, or puncture siding, diminishing the home's aesthetic and protective barrier. Vinyl siding is particularly vulnerable to cracking in high winds, while wood siding may split or warp. Missing or damaged siding can lead to water infiltration, which risks mold growth and structural damage over time. Immediate inspection and repair are crucial to maintaining the home's durability and energy efficiency.

Each year, 1 in every 20 insured homes file an insurance claim with 98% involving property damage.

(Insurance Information Institute, 2021. Claim average from 2017-2021.)

Public Adjusters are licensed insurance professionals trained to interpret your policy, scope and estimate losses, submit your claim, and negotiate with your insurance company to ensure maximum settlement amounts.